SBA 7(a) loans are small business loans that are majority guaranteed for the lender by the U.S. federal government. This is handled by the Small Business Administration (SBA), which is a federal agency intended to promote small business success in the U.S. SBA 7(a) loans are offered and funded by banks and other lenders (just like conventional loans), but as long as the lender follows SBA guidelines, the SBA will guarantee most of the value of the loan for them (75% guaranteed for 7(a) loans >$150,000 in value), regardless of the loan’s outcome. The SBA taking on the majority of the loan’s risk greatly reduces the risk for the lender, allowing them to provide loans to a wider array of borrowers.

SBA 7(a) business loans are limited to loan values under $5,000,000, perfect for small businesses. They have a prepayment penalty of three years, which is shorter than most conventional loans. This means that you can pay off the full balance of the loan after you’ve had it for only three years, making refinancing the loan a possibility in the near future.

Loan Amount

Up to $5,000,000

Down Payment

Minimum (and typical) down payment of 10%

Interest Rate

Based on the prime rate, typically ranging from prime + 1 to prime + 3

Term

25 years for loans involving real estate, 10 years for loans not involving real estate

Collateral

All available collateral, but not required to be fully collateralized

Personal Guarantee

A full personal guarantee is required

Amortization

Fully amortized

Prepayment Penalty

Period of three years, with descending penalties of 5%-3%-1%

Uses of Proceeds

SBA 7(a) loan proceeds may be used for a wide range of eligible business purposes, depending on the borrower’s needs and the structure of the transaction. Common uses of proceeds include, but are not limited to:

– Real estate purchase

– Business purchase

– Equipment purchase

– Construction

– Debt refinance

– Working capital

These flexible use-of-proceeds options make SBA 7(a) loan financing a practical solution for businesses seeking to grow, stabilize operations, or improve their overall financial position.

Note: SBA 7(a) loans may not be used for passive real estate investment purposes. This includes both commercial and residential investment properties that are not primarily owner-occupied by the operating business.

Buy

Use an SBA 7(a) loan to finance the purchase of equipment, commercial real estate, or an existing business. Whether you are acquiring owner-occupied property, upgrading essential machinery, or buying a business with growth potential, our team helps simplify the financing process and secure the capital your business needs to move forward.

Build

An SBA 7(a) loan can help fund a variety of business expansion projects, including leasehold improvements, facility renovations, building additions, and ground-up construction. Our team works closely with borrowers to structure financing solutions that support both immediate construction needs and long-term business goals.

Expand

If your company is ready for growth, SBA 7(a) loan can provide the working capital and long-term funding needed to expand operations. From opening a new location to increasing capacity, hiring staff, or investing in new resources, we offer tailored loan solutions designed to help small businesses scale with confidence.

Top States

SBA 7(a) loans are a popular small business financing option in states all across the United States. In FY 2025, the states with the greatest SBA 7(a) financing volume were:

- California

- Texas

- Florida

- New York

- Georgia

- Illinois

- Ohio

- Colorado

- New Jersey

- North Carolina

Top Cities

From New York to Los Angeles, SBA 7(a) loans help small businesses access financing. In FY 2025, the cities with the greatest SBA 7(a) financing volume were:

- New York

- Los Angeles

- Dallas

- Chicago

- Miami

- Atlanta

- Houston

- Philadelphia

- Denver

- Phoenix

Industries

SBA 7(a) loans can be used across a broad range of for-profit industries, making them one of the most versatile financing options available to small business owners. Whether a business is acquiring property, expanding operations, purchasing equipment, or refinancing eligible debt, SBA 7(a) loans can support many different business models and operating sectors.

Some of the most common industries that use SBA 7(a) business loans include:

– Hotels/Motels/B&Bs

– Dentists

– Private Schools

– Office buildings

– Restaurants

– Retail stores

– Storage facilities

– Car washes

In addition, SBA 7(a) loans are frequently used by service businesses, light manufacturing companies, medical practices, franchise operators, and other owner-operated businesses. The program is designed to support businesses with legitimate operating purposes, as long as they meet SBA eligibility requirements.

Because of its flexibility, the SBA 7(a) loan program is often a strong fit for businesses that need capital for acquisition, expansion, real estate, equipment, or ongoing working capital needs.

SBA 7(a) Loan Qualifications

To be considered for SBA 7(a) loan, the business must meet basic eligibility standards established for small business applicants. In general, qualifying borrowers must own and operate a for-profit business located in the United States or its territories.

Eligible businesses are typically structured as one of the following legal entities:

– Sole proprietorship

– Corporation

– Partnership

– Limited liability company (LLC)

These foundational requirements help determine whether a business may qualify for an SBA 7(a) business loan for purposes such as working capital, business acquisition, commercial real estate, equipment, or expansion financing.

Important note:

Meeting these basic requirements does not guarantee approval. Final SBA 7(a) loan eligibility also depends on factors such as the type of business, use of proceeds, credit profile, repayment ability, and overall lender underwriting criteria.

Benefits of an SBA 7(a) Loan

An SBA 7(a) loan offers several advantages for small business owners who need affordable, flexible financing. Compared with many traditional business loan options, the program is designed to make access to capital more manageable and sustainable over the long term.

Key benefits of SBA 7(a) business loans include:

– Extended repayment terms that are often longer than conventional business loans

– Lower equity injection requirements, helping preserve cash at closing

– Competitive interest rates for a variety of business purposes

These features make SBA 7(a) loans a strong option for businesses seeking financing for commercial real estate, business acquisition, equipment purchases, working capital, refinancing, or expansion. With lower upfront cash requirements and longer amortization periods, borrowers benefit from improved monthly payment affordability and better cash flow management.

Fiscal Year 2025

78,078

7(a) Loans Approved

$37 Billion+

Total Value of Approved 7(a) Loans

SBA 7(a) Loans: Pros and Cons

SBA 7(a) loans have many benefits, including their broad accessibility and flexibility and favorable terms, as well as some drawbacks, including a maximum loan amount of $5,000,000 and slightly higher interest rates than other types of loans.

SBA 7(a) Loans vs. Other Types of Loans

SBA 7(a) Loans vs. Conventional Loans

SBA 7(a) loans and conventional loans are popular financing options for small businesses. However, they’re different in many ways.

SBA 7(a) loans are attainable by a wider array of borrowers than conventional loans due to their government guarantee, and have longer, fully amortized terms, lower down payments – 10% vs. the 20-30% typical of a conventional loan – and often lower monthly payments than conventional loans. However, conventional loans have a quicker loan process, are available from more lenders, don’t have a cap on their size, and can offer lower interest rates for qualified borrowers.

Conventional loans are often the better fit for businesses and borrowers that qualify for them and can afford the larger down payment. If a business is stable, has great cash flow, and can afford a 2-3x larger down payment, it may be able to get a conventional loan from a good lender with a good interest rate. However, for all other businesses and borrowers – those with cash flow that’s anything other than great, those who can’t afford a 20-30% down payment, or those who want reliability, with relatively stable monthly payments over a long, fully amortized loan term – SBA 7(a) loans are the better option.

SBA 7(a) Loans vs. SBA 504 Loans

SBA 7(a) loans and SBA 504 loans are popular financing options for small businesses. However, even though they’re both SBA loans, they’re different in many ways.

SBA 7(a) loans are much more flexible, a single loan from a single lender that can be used for real estate, business acquisition, equipment, working capital, construction, debt refinancing, or a combination of purposes. However, their cap at $5 million precludes their use for larger, more expensive real estate purchases and construction projects. SBA 504 loans, by contrast, are specifically designed for large, fixed asset purchases, primarily commercial real estate and major equipment. Its structure is more complex: a 504 loan is actually two loans bundled together, one from a conventional lender (50% of the project cost) and one from a Certified Development Company, or CDC (40% of the project cost), with the borrower contributing the remaining 10% as a down payment.

The terms reflect these structural differences. SBA 7(a) loans carry variable interest rates based on the prime rate (typically prime + 1 to prime + 3). SBA 504 loans, meanwhile, offer a lower, fixed interest rate on the CDC portion, leading to a lower rate for the loan as a whole and relative long-term rate certainty. However, 504 loans come with significantly longer prepayment penalty periods – often 10 years or more on the CDC portion, compared to just three years for a 7(a) loan. This makes the 7(a) far more flexible for borrowers who may want to refinance, sell, or pay off the loan early.

SBA 7(a) loans are the better fit for most small business borrowers due to their flexibility, simpler structure, and shorter prepayment penalty. They’re especially well-suited for borrowers who want a single streamlined loan, may need to combine real estate with other uses of proceeds, or value the ability to refinance after three years. SBA 504 loans are the better fit for any fixed asset loan where the borrower is confident they’ll hold the property long-term and wants to take advantage of the lower fixed rate on the CDC portion of the loan, especially if the loan is over $5 million.

SBA 7(a) Loan Program History

The U.S. Small Business Administration’s 7(a) loan program has played a key role in fostering the growth and development of small businesses across the country since its creation as part of the 1953 Small Business Act. This bill also created the SBA as a whole, and the program was named after the part of the bill that detailed the program, Section 7(a). The SBA 7(a) loan program was designed to provide financial support to small businesses, which often face difficulties in accessing capital from traditional lending sources.

Over the years, the SBA 7(a) loan program has evolved to become the SBA’s flagship initiative, offering a variety of loan products to assist small businesses with their financing needs. In most years, the program breaks even, as the low default rate on SBA 7(a) business loans means that revenue from SBA processing fees is usually larger than the total value of paid-out guarantees. The program has been instrumental in job creation, economic growth, and entrepreneurship, supporting small businesses in various industries. Its success has made it a cornerstone of the SBA’s efforts to promote small business development and solidified its place in the storied history of American entrepreneurship.

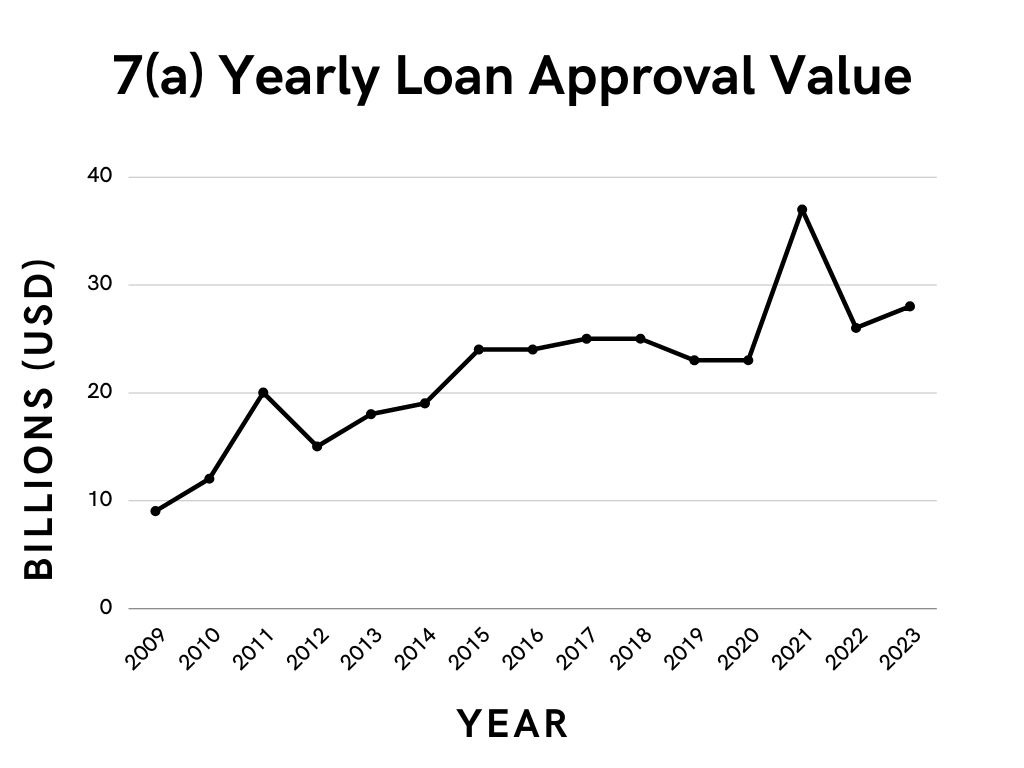

SBA 7(a) Loan Program Statistics

These are the year-by-year* statistics of the SBA 7(a) loan program from Fiscal Year 1992 to today, including the number of 7(a) loans approved and total approval amount.

| Fiscal Year | Loans Approved | Approval Amount |

| 1992 | 23,655 | $5,880,429,292 |

| 1993 | 26,291 | $6,690,995,672 |

| 1994 | 36,049 | $8,142,444,017 |

| 1995 | 55,548 | $8,251,957,812 |

| 1996 | 45,853 | $7,694,062,736 |

| 1997 | 45,288 | $9,461,352,612 |

| 1998 | 42,271 | $9,016,559,155 |

| 1999 | 43,634 | $10,146,109,913 |

| 2000 | 43,748 | $10,523,436,538 |

| 2001 | 42,958 | $9,894,022,393 |

| 2002 | 51,666 | $12,208,026,875 |

| 2003 | 67,306 | $11,268,200,031 |

| 2004 | 81,133 | $13,571,560,391 |

| 2005 | 95,900 | $15,223,525,886 |

| 2006 | 97,291 | $14,525,100,339 |

| 2007 | 99,606 | $14,292,141,213 |

| 2008 | 69,437 | $12,671,235,790 |

| 2009 | 41,288 | $9,191,044,339 |

| 2010 | 47,000 | $12,406,048,700 |

| 2011 | 53,710 | $19,640,298,400 |

| 2012 | 44,376 | $15,153,504,000 |

| 2013 | 46,395 | $17,865,672,500 |

| 2014 | 52,044 | $19,190,547,800 |

| 2015 | 63,461 | $23,583,863,400 |

| 2016 | 64,074 | $24,128,426,343 |

| 2017 | 62,430 | $25,447,458,500 |

| 2018 | 60,354 | $25,372,539,100 |

| 2019 | 51,907 | $23,175,811,000 |

| 2020 | 42,298 | $22,549,825,700 |

| 2021 | 51,856 | $36,536,756,800 |

| 2022 | 47,678 | $25,693,805,700 |

| 2023 | 57,362 | $27,515,666,000 |

| 2024 | 70,242 | $31,124,036,200 |

| 2025 | 78,078 | $37,287,816,200 |

Source: SBA, 7(a) & 504 FOIA

*U.S. Federal Government fiscal years

SBA 7(a) Loans On the Rise

The SBA 7(a) loan program has seen outstanding recent growth, with the annual total value of approved loans tripling in the last 15 years. Not bad for a program that’s been around since 1953!